Investing in rental properties is one of the most reliable ways to build long-term wealth, but getting there requires the right financing. Whether you are buying your first rental or adding to an existing portfolio, understanding your mortgage options can make a big difference in how fast you grow and how much you keep in your pocket.

At Real Estate Investor Friendly Loans, we work with real estate investors across Michigan and 43 states, providing investor-focused mortgage solutions built around cash flow strategies rather than traditional income verification.

What is a Rental Property Mortgage?

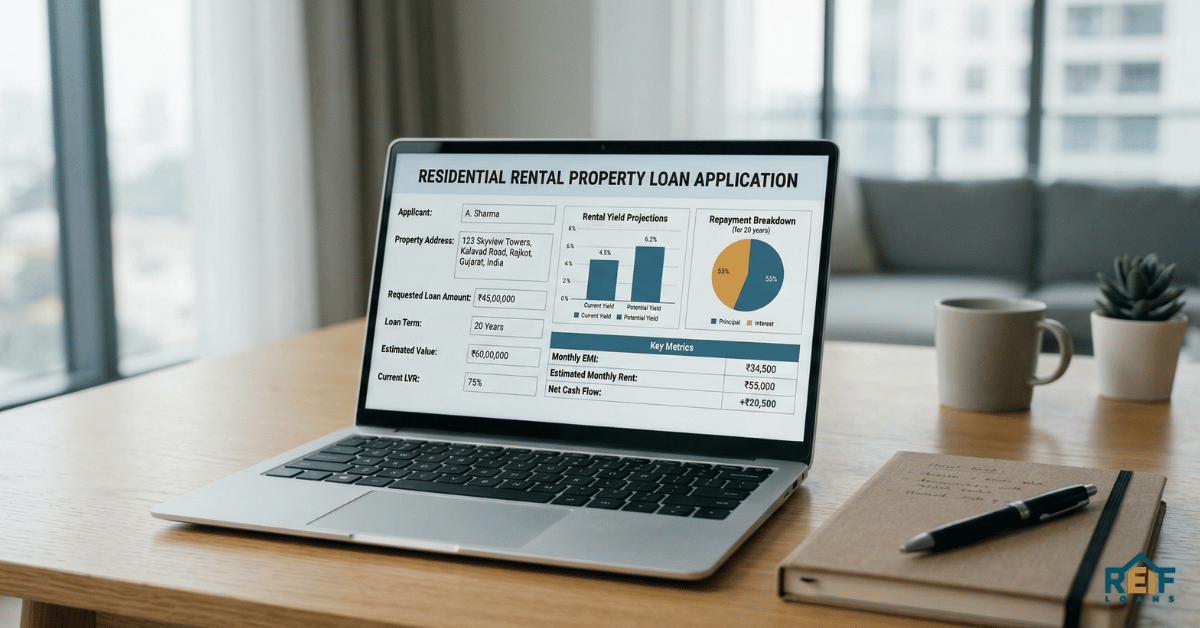

Rental property loans are financing products specifically designed for income-producing real estate. Unlike a primary residence mortgage, these mortgages are evaluated based on the property’s ability to generate income, the investor’s overall financial picture, and sometimes the asset itself, rather than a W-2 paycheck.

Because rental properties carry a different risk profile than owner-occupied homes, lenders typically apply stricter requirements around down payments, credit scores, and cash reserves.

How Lenders Qualify You for a Rental Property Mortgage

Before choosing a mortgage product, it helps to understand what lenders are actually looking at.

Down Payment

Most rental property mortgages require a minimum of 20% down, though some conventional programs may allow 15%. A larger down payment generally means better interest rates and easier approval. At Real Estate Investor Friendly Loans, some products are structured to work with investors who want to preserve more of their capital.

Cash Flow

Many investor-focused lenders, including Real Estate Investor Friendly Loans, look at the property’s rental income rather than your personal earnings. This is the foundation of DSCR-based lending, where the property’s income must cover the debt payments by a required ratio.

Your Credit Profile

Credit score thresholds vary by mortgage type. Conventional mortgages typically require 680 or higher. Non-QM and Real Estate Property DSCR Loan can be more flexible, but stronger credit still works in your favor for rate and terms.

Types of Rental Property mortgages

There is no single mortgage product that works for every investor. Here is a breakdown of the most common options:

Real Estate Property DSCR Loan (Debt Service Coverage Ratio)

Real Estate Property DSCR loans are one of the most practical tools for real estate investors today. Qualification is based on the property’s monthly rental income compared to its monthly debt obligation, not your tax returns or employment status. This makes them ideal for self-employed investors or those with complex income profiles.

Real Estate Investor Friendly Loans specializes in DSCR lending and works with investors to find structures that support long-term portfolio growth.

Conventional Investment Property mortgages

These are standard mortgage products offered through traditional lenders. They typically require:

- Minimum 15 to 20% down payment

- Credit score of 680 or higher

- Documented income through pay stubs or tax returns

- Cash reserves covering several months of payments

They work well for investors with a straightforward financial profile who are buying one or two properties.

Hard Money Loans

Hard money loans are short-term, asset-based mortgages used primarily for fix-and-flip projects or when speed is critical. They close faster than conventional products but come with higher interest rates and shorter repayment windows. Real Estate Investor Friendly Loans offers hard money solutions for investors who need to move quickly on an opportunity.

Real Estate Property Non-QM Loan

Non-QM (non-qualified mortgage) mortgages are designed for borrowers who fall outside traditional lending guidelines. This includes investors with variable income, foreign nationals, or those who prefer bank statement qualification over tax return documentation. These products give investors more flexibility without sacrificing access to competitive terms.

Commercial Real Estate mortgages

Once investors move into multi-unit properties, mixed-use buildings, or larger commercial assets, commercial real estate mortgage come into play. These are structured differently from residential products and are often evaluated on the property’s income potential and overall value. Real Estate Investor Friendly Loans has experience structuring commercial deals alongside residential investment portfolios.

Cash Out Refinance for Investors

One strategy many experienced investors use is the cash out refinance. If you have built equity in an existing rental property, you can refinance for a higher mortgage amount and take the difference as cash. That capital can then be used to fund a new acquisition, cover repairs, or pay down higher-interest debt.

This approach lets investors recycle equity without selling properties, keeping their portfolio intact while still accessing liquidity. Real Estate Investor Friendly Loans help investors evaluate whether a cash-out refinance fits their current strategy and long-term goals.

Choosing the Right mortgage for Your Strategy

Not every mortgage fits every investor. Here are a few factors to think through before applying:

- Investment timeline: Are you holding long term or planning to sell within a year or two?

- Income documentation: Do you have traditional W-2 income or is your income self-directed or variable?

- Portfolio size: Are you financing one property or building toward five, ten, or more?

- Speed requirements: Do you need to close quickly to win a deal?

Real Estate Investor Friendly Loans takes an advisory-first approach, walking investors through product options based on their specific situation rather than fitting everyone into the same box.

Why Investors Work With Real Estate Investor Friendly Loans

Founded by Elizabeth Shvartsman, Real Estate Investor Friendly Loans was built specifically for real estate investors, not for buyers purchasing a home to live in. That distinction shapes everything from how we evaluate applications to how we structure mortgages products.

Here is what sets Real Estate Investor Friendly Loans apart:

- Specialization in Real Estate Property DSCR Loans, non-QM products, hard money, and commercial real estate financing

- Serving investors across Michigan and 43 states

- Transparent lending with clear terms and no hidden surprises

- Fast pre-qualification so investors can move when opportunities appear

- Long-term portfolio perspective built into every conversation

If you are financing a single rental or scaling a multi-property portfolio, having a lender who understands investor goals makes the process significantly smoother.

Common Questions About Rental Property Loans

Can I qualify without showing personal income? Yes. Real Estate Property DSCR Loans and certain non-QM products qualify based on property cash flow or bank statements rather than personal income documentation.

What credit score do I need? It depends on the product. Conventional mortgages generally require 680 or higher. DSCR and Real Estate Property Non-QM Loans may work with lower scores depending on other factors.

How fast can I get pre-qualified? Real Estate Investor Friendly Loans offers a fast pre-qualification process so you know where you stand before making an offer.

Ready to Finance Your Next Rental Property?

Whether you are exploring your first investment property or adding to a growing portfolio, Real Estate Investor Friendly Loans has the products and expertise to support your next step. Connect with our team to discuss your goals and find the mortgages structure that fits your strategy.