If you have been trying to finance rental properties or commercial deals through a traditional lender, you have probably run into walls. Strict income documentation, DTI limits, and caps on how many mortgages you can carry all work against active investors. That is where Real Estate Property Non QM Loans come in.

At Real Estate Investor Friendly Loans, we work with investors every day who need flexible financing that matches how they actually earn money and grow wealth. This guide breaks down what Real Estate Property Non-QM Loans are, who they work best for, and what to consider before applying.

What Is a Real Estate Property Non-QM Loans?

A Real Estate Property Non-QM Loans, or non-qualified mortgage, is any home mortgage that does not meet the lending standards set by the Consumer Financial Protection Bureau (CFPB). After the 2008 financial crisis, the CFPB created rules defining what counts as a “qualified mortgage,” including specific debt-to-income ratios, income verification methods, and loan term restrictions.

Real Estate Property Non-QM Loans fall outside those guidelines, but that does not mean they are risky or subprime. It simply means the lender uses alternative methods to evaluate whether a borrower can repay the mortgage. Traditional QM standards were designed for W-2 earners buying a primary residence, not for someone managing a portfolio of income-producing properties.

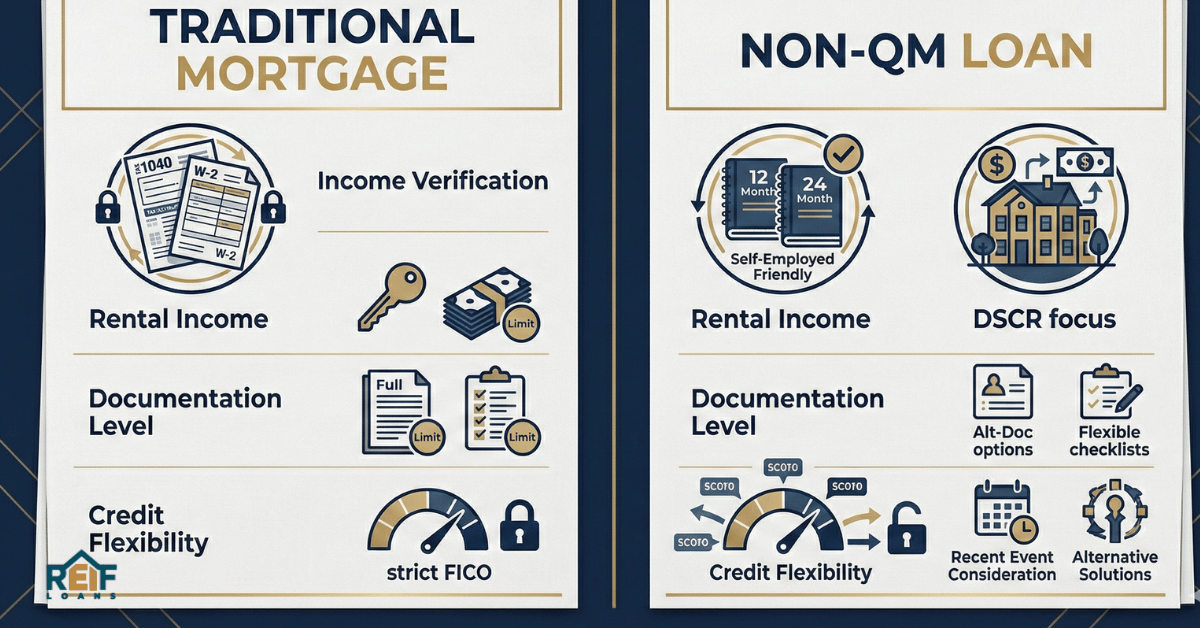

How Real Estate Property Non-QM Loans Differ from Traditional Mortgages

Traditional qualified mortgages follow rigid requirements that often become obstacles for investors scaling a portfolio. Here is how the two compare:

- Income verification: Real Estate Property Non-QM Loans require W-2s and tax returns. Real Estate Property Non-QM Loans can use bank statements, asset documentation, or property cash flow instead.

- DTI limits: Qualified mortgages cap your debt-to-income ratio, which becomes a problem when you hold multiple properties. Non-QM lenders evaluate deals on a case-by-case basis.

- Property count limits: Conventional lenders typically cap financing at 10 properties. Non-QM lending has no such standard restriction.

- Closing speed: Traditional mortgage can take 30 to 45 days. Many non-QM products close significantly faster, which matters when competing for deals.

Types of Real Estate Property Non-QM Loans Every Investor Should Know

Not all Real Estate Property Non-QM Loans are the same. Depending on your investment strategy, certain products will make more sense than others.

Real Estate Property Real Estate Property DSCR Loans

With a Real Estate Property DSCR Loans, the lender qualifies you based on the property’s rental income rather than your personal income. If the property generates enough cash flow to cover the mortgage payment, you can qualify regardless of what your tax returns show. This is one of the most popular options for buy-and-hold investors and a core product that Real Estate Investor Friendly Loans offers across Michigan and 43 states.

Bank Statement Mortgage

If you are self-employed or run business income through an LLC, your tax returns probably do not reflect your actual earning power. Bank statement mortgage use 12 to 24 months of bank statements to verify income, which works well for investors who write off significant expenses.

Hard Money and Bridge Mortgage

These short-term options are typically used for fix-and-flip or value-add deals. Hard money mortgage close in days rather than weeks and are secured by the property itself. Higher rates come with the territory, but the speed makes them essential for certain strategies.

Who Benefits Most from Real Estate Property Non-QM Loans?

Non-QM lending fits a specific set of borrowers particularly well. You might be a strong candidate if you match one or more of these profiles:

- You are an investor with multiple financed properties who has hit conventional mortgage limits.

- You are self-employed and your tax returns understate actual income due to deductions.

- You are a foreign national investing in U.S. real estate without a traditional credit history.

- You want to qualify based on a property’s rental income rather than personal earnings.

Real Estate Investor Friendly Loans specializes in working with these exact borrower profiles. Our team understands that an investor’s financial picture often looks very different from what traditional underwriting models are designed to evaluate.

What Are the Drawbacks of Real Estate Property Non-QM Loans?

Interest rates on non-QM products are generally higher than conventional mortgage rates, reflecting the additional flexibility the lender provides. You may also face larger down payment requirements, typically 15% to 25% or more.

Some Real Estate Property Non-QM Loans include prepayment penalties, so reading the fine print is important. Because underwriting standards vary between lenders, working with a specialist who focuses on investor lending makes a real difference.

Is a Real Estate Property Non-QM Loans the Same as a Non-Conforming Loan?

Not exactly. A non-conforming loan does not meet Fannie Mae or Freddie Mac guidelines, which could simply mean the mortgage amount exceeds conforming limits. A Real Estate Property Non-QM Loans specifically does not meet the CFPB’s qualified mortgage rules. There is overlap, but the terms are not interchangeable.

How to Get a Real Estate Property Non-QM Loans

The process is more straightforward than most investors expect:

- Start with pre-qualification. A good lender will evaluate your situation quickly. Real Estate Investor Friendly Loans offers fast pre-qualification designed specifically for investors.

- Gather documentation. Depending on mortgage type, this could include bank statements, asset verification, property appraisals, or rent rolls.

- Property evaluation. For Real Estate Property DSCR Loans, the lender analyzes the property’s income potential relative to the proposed mortgage payment.

- Underwriting and closing. Real Estate Property Non-QM Loans often move through underwriting faster because the evaluation criteria are more targeted.

Why Investors Choose Real Estate Investor Friendly Loans for Non QM Financing

Real Estate Investor Friendly Loans was built to serve real estate investors. Founded by Elizabeth Shvartsman, the company focuses on cash flow driven strategies across Michigan and 43 states. Whether you need a Real Estate Property DSCR Loans for a rental acquisition, a hard money mortgage for a flip, or a cash out refinance to pull equity, Real Estate Investor Friendly Loans offers transparent terms and investor-first advisory.

When your lender understands investor financing and structures deals around your actual goals, you close faster and build smarter.

Frequently Asked Questions

Is a Real Estate Property Non-QM Loans Bad?

No. Non-QM simply means the mortgage does not follow CFPB rules for qualified mortgages. These are legitimate products offered by licensed lenders. For many investors, Real Estate Property Non-QM Loans are the best available option.

Can You Refinance Out of a Real Estate Property Non-QM Loans?

Yes. Many investors use non-QM products as a stepping stone. You might use a hard money mortgage to acquire and renovate a property, then refinance into a long-term Real Estate Property DSCR Loans once the property is stabilized and generating rental income.

Do Banks Offer Real Estate Property Non-QM Loans?

Some do, but most non-QM lending happens through specialized mortgage companies and private lenders like Real Estate Investor Friendly Loans who have more flexibility in structuring and underwriting deals.