Most mortgage lenders want to see your tax returns, pay stubs, and employment history. DSCR lenders take a different approach. They look at the rental property itself and ask one simple question: does this investment generate enough income to cover the mortgage?

That’s what the Debt Service Coverage Ratio tells them. And if you’re a real estate investor looking to qualify based on property cash flow instead of personal income, understanding this number is critical. Run the calculation wrong, and you might chase deals that will never get approved. Run it right, and you’ll know exactly which properties make financial sense before you ever submit an application.

What Is DSCR and Why Should Investors Care?

DSCR stands for Debt Service Coverage Ratio. It measures the relationship between a property’s income and its debt obligations. Lenders use this ratio to determine if a rental property can pay for itself without relying on your personal finances.

For real estate investors, this matters because Real Estate Property DSCR Loans don’t require W2s, pay stubs, or employment verification. Whether you’re self-employed, have complex tax write-offs, or simply want to qualify based on property performance, DSCR lending offers a practical path to financing. Real Estate Investor Friendly Loans specializes in these investor-focused mortgage solutions across Michigan and 43 other states.

The Basic DSCR Formula

The formula itself is straightforward:

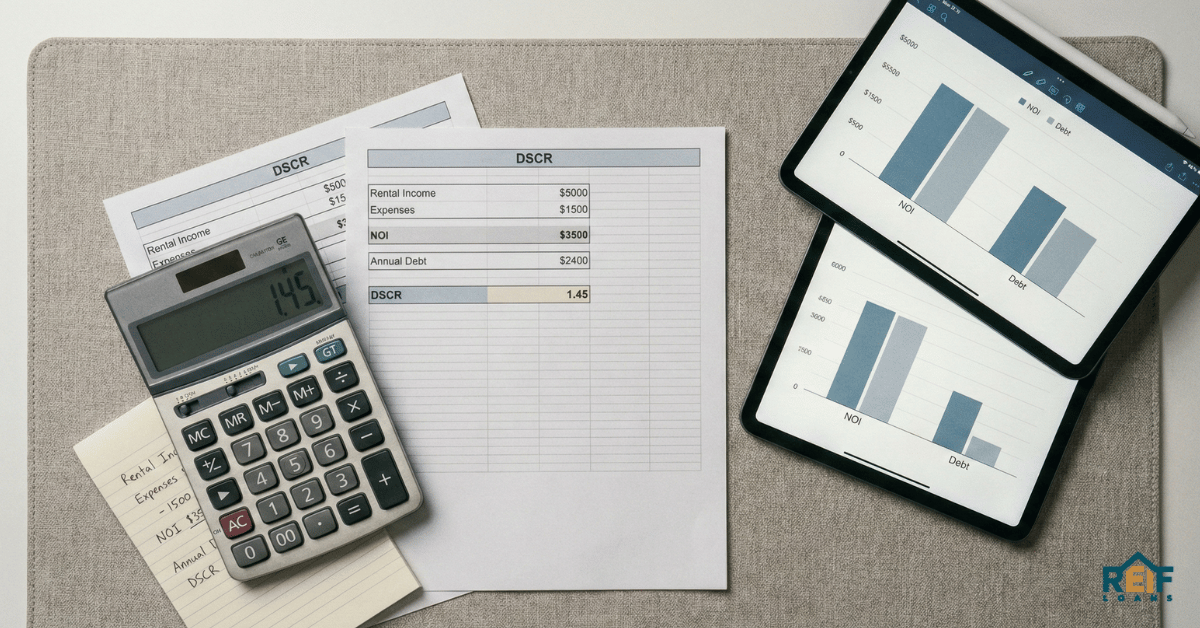

DSCR = Net Operating Income (NOI) ÷ Total Debt Service

Here’s what each component means:

- Net Operating Income (NOI): The annual rental income your property generates after subtracting operating expenses

- Total Debt Service: Your total annual mortgage payment including principal, interest, taxes, and insurance (often called PITI)

The result tells you how many times over your property income covers the mortgage. A DSCR of 1.0 means you break even. Above 1.0 indicates positive cash flow, while below 1.0 means the property doesn’t fully cover its debt.

How to Calculate DSCR Step by Step

Let’s walk through each step so you can run this calculation on any investment property you’re considering.

Step 1: Determine Your Gross Rental Income

Start with the monthly rent your property generates or could generate. If you already have a tenant, use the actual lease amount. For properties without existing leases, lenders typically use fair market rent determined by an appraiser.

Multiply your monthly rent by 12 to get your annual gross rental income. For example, a property renting at $2,000 per month produces $24,000 in annual gross income.

Step 2: Calculate Net Operating Income

Some lenders simplify this step and use gross rent directly. Others subtract operating expenses to arrive at NOI. Common expenses include:

- Property management fees (typically 8-10% of rent)

- Vacancy allowance (often 5-10%)

- Maintenance and repair reserves

- HOA fees if applicable

- Property taxes and insurance (if not included in debt service)

For this guide, we’ll use the simplified approach most DSCR lenders prefer, which uses gross rental income as the numerator.

Step 3: Calculate Total Debt Service

Add up all the components of your annual mortgage payment:

- Principal payment

- Interest payment

- Property taxes

- Homeowners insurance

- HOA dues (if applicable)

- Flood insurance (if required)

Take your total monthly PITI payment and multiply by 12. If your monthly payment is $1,600, your annual debt service equals $19,200.

Step 4: Apply the Formula

Divide your annual rental income by your annual debt service. Using our example numbers:

$24,000 ÷ $19,200 = 1.25 DSCR

This property has a DSCR of 1.25, meaning it generates 25% more income than needed to cover the mortgage.

DSCR Calculation Examples

Seeing real numbers helps clarify how this works in practice. Here are three scenarios investors commonly encounter.

Example 1: Strong Cash Flow Property

A single-family rental in Grand Rapids, Michigan has these numbers:

- Monthly rent: $2,200

- Annual rental income: $26,400

- Monthly PITI: $1,650

- Annual debt service: $19,800

DSCR Calculation: $26,400 ÷ $19,800 = 1.33

This property easily qualifies for most Real Estate Property DSCR Loan programs with strong cash flow.

Example 2: Break-Even Scenario

A duplex generates the following:

- Monthly rent: $3,000 (both units combined)

- Annual rental income: $36,000

- Monthly PITI: $2,950

- Annual debt service: $35,400

DSCR Calculation: $36,000 ÷ $35,400 = 1.02

This property barely breaks even. Some lenders accept 1.0 DSCR, but you may face higher rates or need additional reserves.

Example 3: Negative Cash Flow

A condo investment shows these figures:

- Monthly rent: $1,800

- Annual rental income: $21,600

- Monthly PITI plus HOA: $2,100

- Annual debt service: $25,200

DSCR Calculation: $21,600 ÷ $25,200 = 0.86

This property has negative cash flow. To qualify, you’d need a larger down payment to reduce the mortgage amount or find a lender that accepts sub-1.0 DSCR ratios.

What DSCR Do Lenders Require?

Requirements vary by lender, but here are common thresholds:

- 1.25+ DSCR: Best rates and terms, easiest approval

- 1.0 to 1.24 DSCR: Standard approval with competitive rates

- 0.75 to 0.99 DSCR: Some lenders allow this with lower LTV or higher reserves

- Below 0.75 DSCR: Difficult to finance without significant compensating factors

Real Estate Investor Friendly Loans works with investors across the DSCR spectrum, offering flexible solutions for rental property financing and commercial real estate mortgages tailored to your investment strategy.

Tips to Improve Your DSCR Before Applying

If your DSCR falls short of lender requirements, you have several options:

- Increase your down payment to lower the mortgage amount and monthly debt service

- Raise rents to market rate if you’re currently below market

- Shop for better insurance rates to reduce your PITI

- Consider interest-only mortgage options, which lower monthly payments

- Choose a different property with better income-to-debt ratios

Final Thoughts

Calculating DSCR before you apply for financing helps you understand exactly where you stand. It also lets you compare multiple properties objectively based on their cash flow potential rather than gut feelings.

Whether you’re purchasing your first rental property or expanding a growing portfolio, understanding this ratio puts you in a stronger position. Real Estate Investor Friendly Loans offers fast pre-qualification for Real Estate Property DSCR Loans and investment property financing, helping real estate investors across Michigan and 43 states finance, refinance, and scale with confidence. Reach out today to discuss your next investment.